John Maynard Keynes is the grandfather of all modern mainstream economic thought. Richard Nixon was famously attributed as saying, “We are all Keynesians now” whilst slamming shut the gold window and launching the era of global fiat money. (Nixon didn’t really say this, it was actually Milton Friedman)

The phrase came back in vogue in the aftermath of the Global Financial Crisis when neo-Keynesians like Paul Krugman called for, and got, massive government and Central Bank intervention into the global economy in order to “save it”.

Back in 1930, Keynes looked out into the future and saw that with the proper management of the economy, monetary policy and the like, the world could attain a type of utopian stasis:

Keynes, working in 1930, expected growth to come to an end within two to three generations, and the economy to plateau. He referred to this imaginary state of equilibrium as “bliss”.

— Nick Gogerty, “The Nature of Value”

In his essay “The Economic Possibilities of Our Grandchildren” Keyne’s imagined the big challenges of our days in the 21st century would be what to do with all that extra leisure time and how to achieve fulfillment since by now the quest for wealth and material gain would become more or less unfashionable or even obsolete.

“Thus for the first time since his creation man will be faced with his real, his permanent problem – how to use his freedom from pressing economic cares, how to occupy the leisure, which science and compound interest will have won for him, to live wisely and agreeably and well.”

Granted, Keynes did say this would happen if mankind avoided any calamitous wars and if there was no appreciable increase in population. Two more flawed base assumptions there could not have been.

But this hasn’t stopped the world’s conventional economists, not to mention the political and policy-making class (a.k.a The Overlords) from embracing the uniquely Keynesian notion that if you just know which macro-economic levers to pull, and how much and for how long, and when to do it; then you can get just the right amounts of: money quantity, money velocity, interest rates, nominal inflation, savings rates, capital expenditures, unemployment levels and consumer spending to make Everything Just Right All The Time without ever having so much as a downtick or a speed-wobble, ever again.

(In case you were interested, it looks something like this: K¢ = [B – U(C)]/U¢)

Converging on Bliss

The formula I linked above comes from a page examining “The Ramsey Exercise” after Frank P. P. Ramsey who published an article in 1928 which Keynes called “one of the most remarkable contributions to mathematical economics ever made”.

Ramsey endeavored to find the optimal rate of savings which would maximize social welfare.

He sought to find the allocation across generations which maximized social welfare — with “social welfare” defined as the sum of utilities of people in a society. From the social welfare-maximizing allocation, we will be able to determine an “optimal” rate (or rather, path) of saving.

Why is this important? Because politicians believe that there is such thing as an optimal rate of savings. While in the past there may have some rumination that it was too low (“myopic agents”), what really bothers Keynesians is if it gets too high, which is why you have things like artificially supressed interest rates – ZIRP without end, and even negative interest rates.

As I lamented in Cronyism in the 21st Century:

These policies are utterly backwards in that they posit what economic forces should do according to some model, instead of trying to understand what they actually do based on observed results.

So according to politicians, pundits and Krugmans, you tweak stuff just right, and you get this:

“Converging on bliss”

If you look at US GDP growth since 1930:

We do see the 5-year moving average coming down to 0. No growth, just like Keynes postulated in 1930. Combine this with Janet Yellen’s revelation that if poor people would just get with the program and accumulate more assets things would be grand and guess what?

We have arrived at Bliss. Doesn’t it feel great?

All Progress is Cybernetic

What anybody who actually examines the issue realizes is that all progress is cybernetic in nature. What this means is that all self-sustaining systems or processes (like an economy or an ecology) employ methodologies for self-regulation, and they rely heavily on evolution in one form or another.

Maxwell Maltz, in his groundbreaking (albeit largely uncredited) antecedent to which the entire modern self-help movement owes it’s existence, Psycho-Cybernetics, stressed that a big component of any system’s progress is that it relies primarily on feedback loops both positive and negative.

The process simply doesn’t work without both negative and positive consequences of past-actions to inform present decisions toward future goals (the original title of this post was “The Extinction of Consequences”)

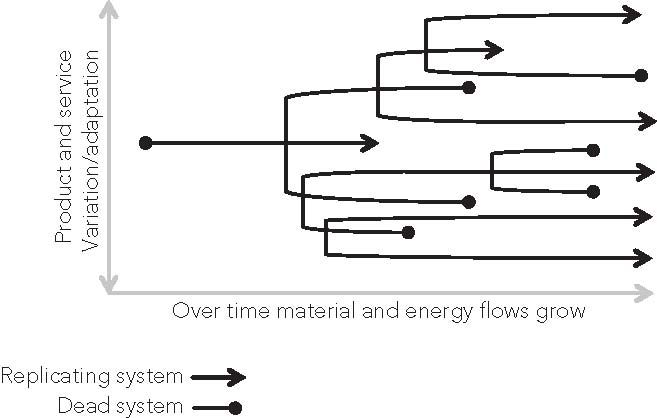

Gogerty’s “The Nature of Value”, shows a chart of a cybernetic process:

The dots indicate dead ends – negative feedback “this doesn’t work” while the arrows indicate paths of “so far, so good”.

What modern economic interventionism attempts to do is eliminate all the dots (and then make sure all the arrows are “equal”). Policy makers and political fixers hold a mechanistic view of the macro economy, implementing “fixes” and managing it because in their minds, it’s just an algorithm.

As Gogerty observes:

“[..]mechanical theories still have adherents, however, and can be dangerous if pursued aggressively using monetary or political force. The only economic systems today that are truly at or close to equilibrium are nearly dead economies. A cow that achieves equilibrium is called a steak, and the economy closest to achieving equilibrium today is North Korea circa 2013”.

The reality is that the economy is a complex adaptive system and thus inherently “unmanageable”. The system itself adapts so you will never come up with anything that achieves “perfect equilibrium”.

Any attempt to do so suppresses the built-in signaling mechanisms and thus all system participants begin to make choices based on “facts” which are increasingly and iteratively distorted by the overlaying policy attempts at eliminating negative feedback.

“Keynes and other economists ignored, dismissed, or seriously misunderstood growth, innovation, value, and adaptive economic processes. Economists mathematic models created the economy like a linear or probabilistic machine.” (ibid.)

And the centrally planned attempts at running the economy as if it were such a linear, probabilistic machine that could be steered shy of recessions or downturns has instead created an escalating sequence of severe dislocations.

- In 2008 had there been no bailouts and the insolvent banks were allowed to die, the economic malaise would have been cleared out within a year or so and a genuine economic recovery could have commenced. (As Stockman exhaustively detailed in The Great Deformation)

- In 2000 had the .COM bubble simply been allowed to burn itself out, with a not-so-bad recession, we would never have had The Housing Bubble in 2008 (which Krugman demanded)

This pattern of intervening to avoid recessions and economic downturns goes all the way back to Nixon’s existential crisis of 1971, perhaps even further – to 1913, when the Fed was created to ensure economic stability for all time.

Today the distortions are now so far advanced that all market signalling is for the most part, totally broken. The stock market reaches new highs on diminishing volume, it costs you money to save your money and there is no official inflation – despite the fact that everything either costs more or it comes in a smaller package for the same price (shrink-flation).

The global financial system is flashing bright red warning lights and yet complacency rules the day and the official policy and media pundit line is that the recovery (now in it’s 5th year) actually exists.

One of these days all of the market signalling mechanisms are going to snap back into functionality and most likely overshoot the mean in a non-linear, disorderly way.

When that happens, the best possible course of action is to not be in the path of one of the gigantic elastic forces snapping back into place at extremely high velocity. Stay out of debt, avoid counter-party risk, be diversified, and have a bug-out plan.

Leave a Reply